European Aviation Shows Signs of Recovery

At the end of 2022, EUROCONTROL published an analysis paper on the recovery of the aviation industry in Europe as well as predictions for 2023. (Photo: EUROCONTROL)

The aviation industry has been transformed as a result of the COVID-19 pandemic. Now, as recovery continues, Eurocontrol has published an analysis paper that breaks down the industry’s current situation and also looks to 2023 for continued recovery and further growth of the commercial sector.

Overall, despite conflict in Ukraine, labor strikes, and inflation, European airlines have demonstrated that travelers across the continent are ready to return to the skies. Around 2 billion passengers were flown in 2022 on 9.3 million flights. This figure still trails behind 2019’s record 11.1 million flights. Additionally, overall traffic levels are still lower compared to previous years, with intra-European traffic still down 15% from 2019. Germany, the United Kingdom, and France have not yet fully recovered, with daily flights 20%, 25%, and 13% lower respectively compared to 2019’s records.

These traffic levels are reflected at Europe’s top ten busiest airports. Frankfurt, first in terms of aircraft movements in 2019, has dropped to fourth busiest in 2022. London-Heathrow, formerly in fourth place, has dropped to fifth while Paris has remained in third. Istanbul, formerly eighth, has climbed to first, and boasts 1,156 average daily aircraft movements.

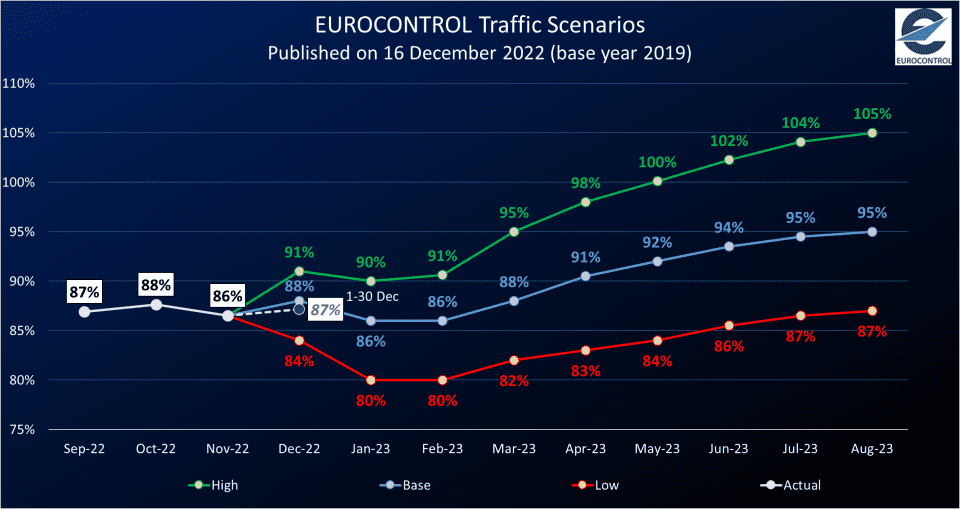

(Photo: EUROCONTROL)

Ryanair is currently the largest aviation group in Europe, with an average of over 2,500 flights per day—a 9% increase from 2019. It is followed by the Lufthansa Group, which operated 2,276 daily flights. Though up from 2021, it still had 31% fewer flights when compared to pre-pandemic operations. These groups are followed by International Airlines Group, Air France-KLM, easyJet, and Turkish Airlines, all of which are operating smaller schedules relative to their historic highs.

The increased passenger volumes, combined with strikes and staffing shortages, have made punctuality a challenge for the airlines of Europe. The average arrival delay increased by 33% from 2019, rising from 12.7 to 16.9 minutes. The average departure delay also rose to 19.6 minutes, up from 15.3 minutes in 2019. Overall, 71.7% of flights arrived on time in 2022, while only 65.9% of flights departed on time. The reliability of Europe’s airlines worsens when looking at the peak travel periods of the year. In fact, fewer than 50% of flights departed on time in July. This figure did not rise above 60% for most of the busy summer season. It is estimated that in 2022, 48% of all delays were caused by staffing and another 25% were delayed because of weather.

Despite struggles with punctuality, many European airlines were able to return to profitability in 2022, and many others were able to narrow their losses and improve their financial positions. Although low-cost carriers have seen some of the most success as recovery continues, Europe’s largest low-cost carrier, Ryanair, was one of the only low-cost carriers to report an operating profit. EasyJet and Wizz Air have seen smaller losses but have yet to pass the breakeven point. Meanwhile, Air France-KLM, International Airlines Group, Lufthansa Group, and Turkish Airlines have all reported profits.

Eurocontrol now expects air traffic to reach 92% of its 2019 levels in 2023 and predicts that it will not fully recover until 2025. Though it anticipates further recovery next year, Eurocontrol also points to punctuality and airspace issues from the conflict in Ukraine as challenges still facing Europe’s airlines.

The post European Aviation Shows Signs of Recovery appeared first on Avionics International.

—————

Boost Internet Speed–

Free Business Hosting–

Free Email Account–

Dropcatch–

Free Secure Email–

Secure Email–

Cheap VOIP Calls–

Free Hosting–

Boost Inflight Wifi–

Premium Domains–

Free Domains